'Money trauma': slippery slope to a cashless society?

A look at what might happen when the language of healing begins to overlap with the language of policy.

The idea of ‘trauma’, once a tightly defined clinical concept caused by exposure to extreme and even life-threatening events, has taken on new meaning in mainstream culture — along with its parallel, ‘post-traumatic stress disorder.’

This has given younger generations a new vocabulary and a new framework to deal with what older generations once just called ‘life’ or ‘the school of hard knocks.’ Trauma has been broadened to include a very wide spectrum of experiences: chronic stress, emotional neglect, financial instability, social rejection, even that series of uncomfortable interactions we all experienced during adolescence. Who among us, by these standards, is left un-traumatized?

This expanding definition is how we ended up with the concept of ‘money trauma,’ and a whole ecosystem of books, podcasts, and TikTok coaches to go along with it.

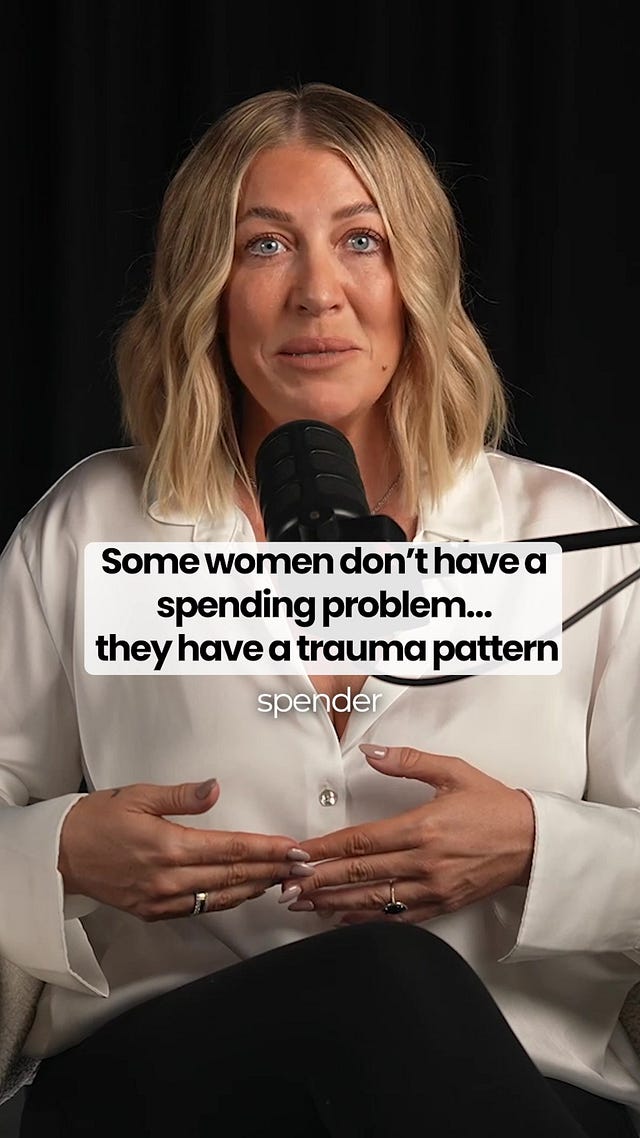

Here’s an example from Jessica Sol, a mentor and “wealth coach” with over 6,000 followers on TikTok:

The trauma spender buys to regulate emotion. She was told “no” too many times growing up, so now she says “yes” to everything she can reach. Having things feels like safety, like proof she’s okay. Or she spends with quiet fury, collecting what she feels owed.

Neither is a flaw. Both are unprocessed wounds playing out inside a bank account that’s trying to tell her the truth.

Tiktok failed to load.

Tiktok failed to load.Enable 3rd party cookies or use another browser

At its core, the premise of money trauma is simple: repeated negative experiences with money — whether caused by poverty, debt, financial instability, overspending, or even inherited attitudes from parents — can shape behavior in ways that resemble trauma responses. A person who hoards money might be described as operating out of fear. Someone who spends too much and refuses to look at their bank balance is framed not as irresponsible but as ‘dysregulated.’

Behavioral economists like Daniel Kahneman and Amos Tversky helped establish the concept that humans are not rational actors when it comes to money, demonstrating how cognitive biases distort financial decision-making. Later, financial therapists — a relatively new profession formalized through organizations like the Financial Therapy Association — began blending psychology with personal finance.

But money trauma as a phrase really gained traction through Instagram therapists, TikTok coaches, and online wellness platforms. There, complex financial realities are reframed as internal emotional landscapes that can be ‘healed.’

In that sense, the phenomenon fits neatly into a broader cultural shift in which structural problems are increasingly translated into personal narratives. If someone is struggling financially, the money trauma framework can shift attention inward — toward beliefs, mindset, and emotional healing — rather than outward, toward wages, inflation, debt structures, or policy decisions. In other words, it can subtly reframe structural economic pressures as personal psychological issues, placing the burden on the individual.

That shift has downstream effects. It changes how responsibility is assigned, how solutions are proposed, and how institutions justify intervention. When discomfort is reinterpreted as damage, the threshold for systemic change lowers. Policies and frameworks that promise to reduce stress, stabilize outcomes, or eliminate uncertainty can be framed as forms of protection or care.

When money itself is described as a source of harm, something that induces anxiety, inequality, and psychological damage, it becomes easier to question its legitimacy as a societal instrument. That doesn’t necessarily lead directly to an argument for the total abolition of cash; but it helps establish that the current form of money is flawed at a human level. Once that premise is accepted, alternative systems begin to appear not as radical, but as compassionate.

This is where ideas like universal basic income and alternative currencies enter the conversation. Universal basic income — discussed often and openly by the Silicon Valley tech bros who brought us AI, automation, and job displacement — then carries a psychological and emotional appeal. If financial instability is a source of widespread distress, guaranteeing income can be positioned as a form of healing.

Concepts like ‘energy-based currencies’ or ‘resource-linked scrips,’ laid out clearly in the Technocracy Study Course of the 1930s, take this idea a step further by questioning whether money should exist at all, and instead proposing systems tied to tangible outputs like energy production or carbon metrics. These ideas still strike many as coming from the realm of science fiction, even though the structural apparatus for them is currently being built in real-time.

Even if we don’t accept these technocratic proposals as inevitable, it’s concerning that the cultural groundwork for them is being laid indirectly. If enough people come to see money as something that distorts behavior, entrenches inequality, and generates chronic stress, the appetite for systemic overhaul increases. In that environment, proposals that once seemed extreme or even dystopian can be reframed as necessary corrections.

As a platform that writes about the slow erosion of life as we once knew it, the Collapse Life team is not blind to the fact that economic precarity, social fragmentation, and constant digital exposure have created conditions that are different than those faced by earlier generations, at least in form if not intensity.

We accept that there is little doubt financial stress can affect mental health, or that early experiences shape future behavior. But the expansion of that reality into a broader narrative that recasts economic systems as trauma-inducing constructs that need to be replaced is where our concerns arise.

Once a system is defined primarily by the harm caused by it, the question is no longer how to reform it, but whether it should exist at all. And history suggests that when that question takes hold at scale, the answers that follow tend to reshape far more than just the system itself.

Talk about a trauma-inducing construct, imagine the harm that we all are going to experience if the technocrats are able to activate their tokenized, social credit induced, monetary control system! Yikes, we all will need therapy! Lol.

It’s interesting that the very economic system that the central bankers put into place and got filthy rich off of, enabling them to even contemplate creating the beast system, is now being vilified as trauma based and a source of widespread distress! Hegelian Dialectic, you think? Now all we need is solution!

It is the perfect storm of the cultural shifts that have come about. First of all is the idea propagated to the world of credit dependence being good and necessary. They have been spreading the idea that there is no reason to save and that things will just take care of themselves. The government will provide for healthcare, retirement, food, and housing.

The narrative has been "You deserve it." Whether it is a vacation, new car, bigger television, a home in a nice place, the fancy clothing and accessories, or whatever. Just attend a college that you can't afford on loans you can't pay and you will get your dream job that will allow you to afford everything that you ever wanted.

Yes, people are traumatized by reality when it hits them. When that happens, it is too late to do anything about it. They are unable to have any money because it is all going to the bank for their car loan and their student loans. It is also going towards the entertainment that they are paying for through subscriptions and things that they have purchased on credit. The destination weddings and vacations.

The bankers and others didn't hold a gun to their heads. They went into it willingly because they believed the fantasy that they were told. They were insulated from the costs by just putting their name on the dotted line on the credit application. It is not a big change that would come from a digital currency. We already have that. There are very few financial transactions that actually involve cash in our modern world. We are just playing with imaginary Monopoly money. Small purchases are just a tap on the card reader. Big purchases are just a signature and an electronic subtraction from one account and an addition to another. If there is not enough money in the account for the transaction, it just gets an automatic loan at a ridiculous interest rate that you never even see. Maybe the payment will just be taken monthly where you pay a penalty every time when there isn't enough money in the account.

I know this because I have lived it. Thankfully, it is all in the past and I recovered from it. It was a very hard lesson though. You have to swim against the current and people think you are crazy for not playing the game that they are playing. You have to learn to do without things for a while. But once you get past the first stages, life becomes much easier.